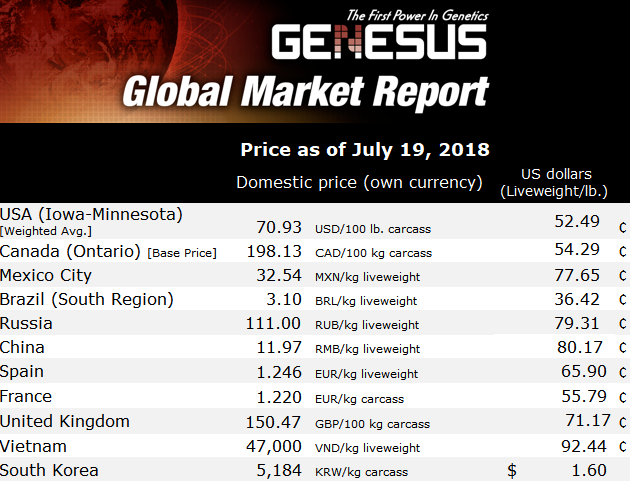

EU and Spanish Pork Markets

Mercedes Vega, General Director for Spain, Italy & Portugal

With 49.6 million market hogs and about 4.25 million tons of pork produced in 2017, Spain is the fourth largest producer of pork in the world.

Last two quarters overview

Currently Spain’s pork producers are surfing around their break-even point. The cost of production for the first six months of 2018 has been around of 1.04–1.05 €/kg ($0.55 USD/lb) average. On the packers side the profit per market hog is between 2.27 and 3.4€ (~$3.28 USD/hog) average.

One concerns for pig producers in Spain is a potential expansion of the swine fever in the EU.

The packing plants are experienced a lot of tension in the market, mainly because of changes on China’s market which has decelerated its pork demand damming the volume of stored pork. There are a lot of uncertainty about pork exports outside the EU causing these lower prices domestically. It seems like right now the packers are starting to lose money.

The usual agreed price between packers and pork producers at the Mercolleida´s bargain table had turned a little uglier over the last month or so. Both sides of the pork industry have found it more difficult to get agreements driven by international markets. So we have in a situation with two faces.

- on one side – there is more demand than offer from the packing plants, since they need to cover a minimum volume in order to avoid higher loses, on the other hand, the packers are facing the frozen storages stock.

- Spain experienced a cool summer so far, in advantage for a faster growth on pigs.

Categorised in: Featured News, Global Markets

This post was written by Genesus